Published on: 2026-04-09

Updated on: 2026-04-09

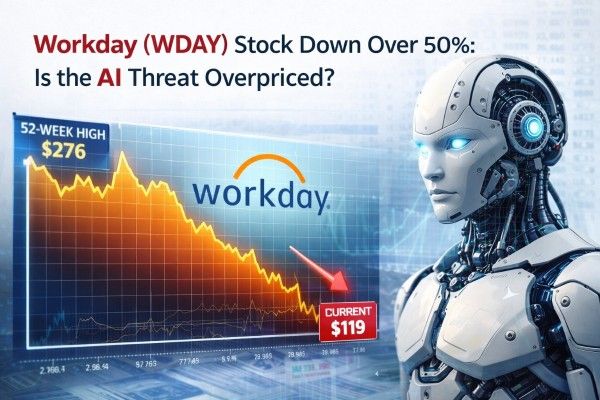

Workday stock was trading near $119 on April 9, 2026, about 61% below the February 26, 2024, record close of $307.21 and roughly 57% below the 52-week high of $276.

The market is discounting a software-wide AI reset after new enterprise AI tools accelerated fears about seat-based SaaS and Workday's own fiscal 2027 subscription growth slowdown to 12%-13 %.

Bearish concerns are valid, as some large enterprise deals are experiencing delays and industry peers are transitioning to usage-based monetization instead of traditional per-seat pricing.

However, these concerns may be overstated. Workday ended fiscal 2026 with 97% gross revenue retention, a $28.1 billion subscription backlog, over $400 million in emerging AI ARR, and AI-linked expansion deals that averaged nearly 50% larger.

The selloff is partly company-specific but also part of a broader 2026 software reset.

Investor concern intensified after new enterprise AI tools revived fears that traditional application vendors could lose pricing power if customers replace workflow-specific interfaces with generalized AI assistants and agents.

Workday reinforced these concerns by projecting fiscal 2027 subscription revenue of approximately $9.925 billion to $9.950 billion, representing 12% to 13% growth, which is below the 14.5% growth achieved in fiscal 2026.

Workday reported that its fiscal Q4 subscription growth was boosted by nearly one percentage point due to the DIA contract, a benefit that will not recur in Q1.

The company also said some net-new large-enterprise deals are taking longer to close, particularly in Federal, state, and local education (SLED), healthcare, and parts of the commercial market.

Management added that most of those opportunities remain active in the pipeline, and a few had already closed in Q1.

This indicates that some of the perceived slowdown is due to timing and challenging year-over-year comparisons, rather than solely AI-driven displacement.

AI has the potential to streamline workflows, reduce manual tasks, and shift value from user access to task completion.

ServiceNow's CEO recently said that about half of new business revenue now comes from non-seat-based models. Meanwhile, Salesforce is framing Agentforce around delivered work and reported $800 million in Agentforce ARR in fiscal 2026.

Workday is also adopting this approach with Flex Credits, though it remains in the early stages of this transition.

| Metric | Latest Figure | Why It Matters |

|---|---|---|

| Fiscal 2026 Total Revenue | $9.552B | Still growing at scale |

| Fiscal 2026 Subscription Revenue | $8.833B | Core recurring base remains durable |

| 12-Month Subscription Backlog | $8.833B | Nearly equals last year’s full subscription revenue |

| Total Subscription Backlog | $28.101B | Roughly 2.94x fiscal 2026 total revenue |

| Gross Revenue Retention | 97% | Renewal durability remains high |

| Fiscal 2026 Non-GAAP Operating Margin | 29.6% | Profitability remains strong |

| Fiscal 2026 Free Cash Flow | $2.777B | Cash conversion is still improving |

| Emerging AI ARR | Above $400M | AI monetization is no longer theoretical |

| Q4 Emerging AI New ACV | Above $100M | AI upsell is scaling fast |

*The table is based on Workday's fiscal 2026 results and management's prepared remarks. The backlog multiple is inferred from reported figures. Note that both 12-month and total subscription backlog include the impact of the Paradox and Sana acquisitions.

The key figure in the table is the 12-month subscription backlog, which stands at $8.833 billion and closely matches Workday’s entire fiscal 2026 subscription revenue. While this does not remove the risk of disruption, it challenges the market’s most pessimistic outlook.

Renewal rates remain stable. That does not rule out future AI pressure, but it does suggest Workday's core base has not yet shown the kind of deterioration implied by the share-price collapse.

Another important factor is revenue mix. Management said net expansion remained consistent through FY26 and contributed roughly 60% of subscription revenue growth for both Q4 and the full year. Medium enterprise customers also drove roughly 60% of net new ACV in FY26.

Existing installations continue to perform well, although new deals are taking longer to secure. The primary challenge is the pace of growth and the shift in monetization, rather than immediate product obsolescence.

Workday’s strategic advantage lies not in AI’s inability to impact HR and finance, but in the continued need for deterministic systems of record for payroll, compliance, permissions, and auditability.

Management’s AI strategy focuses on integrating these governed transaction systems with probabilistic AI, which is particularly credible in HR and finance due to the higher cost of errors compared to lighter SaaS categories.

Monetization evidence is moving from promise to execution. In fiscal 2026, Workday delivered 1.7 billion AI actions and generated more than $100 million in Q4 new ACV from emerging AI products. Management also said overall ARR from those offerings now exceeds $400 million, and that 12 organically developed role-based agents are starting to move into general availability.

Over 400 customers are already using these agents. Early self-service deployments have reduced HR case volume by 25% and increased employee productivity by 20%.

There are additional pricing signals the market may be underweighting. In Q4, AI was involved in roughly half of Workday's customer-base transactions, expansion deals that included AI were nearly 50% larger on average, and nearly 50 customers had signed on to use Flex Credits. That is early evidence of a gradual shift away from pure seat-based monetization.

Using a market capitalization of about $61.97 billion on April 9, 2026, Workday trades at about 6.5x trailing FY26 revenue and about 5.8x rough FY27 revenue, if you combine the subscription guidance midpoint of $9.9375 billion with roughly $710 million of expected professional services revenue.

That is close to Salesforce at about 6.0x trailing revenue and well below ServiceNow at about 14.4x. The market is therefore valuing Workday more like a mature software company than a premium AI platform.

As a result, Workday stock is no longer priced for perfection. In fiscal 2026, Workday’s rule-of-40 profile was approximately 42.7, based on 13.1% revenue growth and a 29.6% non-GAAP operating margin. Salesforce reported about 44.1, while ServiceNow’s framework remains stronger, with growth above 20% and margin guidance near 32%.

In summary, Workday is not valued as a leading AI growth company, but rather as a stable franchise facing ongoing model risk.

| Scenario | Core Thesis | Implied Multiple On Rough FY27 Revenue | Implied Equity Value |

|---|---|---|---|

| Bear Case | AI compresses seat growth, large deals stay slow, monetization shift lags | 5.5x | $58.6B |

| Base Case | Core apps stay sticky, AI cross-sell offsets some seat pressure, growth stays near 12% to 13% | 6.0x | $63.9B |

| Bull Case | Agents accelerate expansion, Flex Credits scale, growth reaccelerates in FY28 | 7.0x to 7.5x | $74.5B to $79.9B |

*The scenario table is based on analytical inferences using Workday’s current market capitalization, fiscal 2027 guidance, and prevailing peer valuation ranges.

With a market capitalization of about $62 billion, Workday stock is trading close to the base-case scenario in this framework. That suggests the market has already priced in meaningful AI-related monetization risk, but not a full franchise break.

A sustained re-rating will likely require evidence that AI can improve revenue quality, not just preserve relevance.

Current data does not indicate this. Retention remains at 97%, the backlog continues to grow, and core subscription revenue is increasing at a double-digit rate.

Evidence would include faster adoption of Flex Credits, increasing AI ARR, consistently high retention rates, and normalization in the timing of large enterprise deals.

The primary risk is that Workday remains relevant but becomes less able to monetize its offerings.

Workday is not experiencing a binary AI-driven extinction. Instead, it is undergoing a transition from charging for access to charging for outcomes, a shift that is transforming the enterprise software landscape.

The stock’s approximately 61% decline from its 2024 high already reflects much of the transition risk. The market now requires evidence that Workday can leverage AI as a growth driver rather than solely as a defensive measure.

Until such evidence is more widespread, the AI threat appears overstated in scale, though it remains a genuine concern.

Disclaimer: This material is for general information purposes only and is not intended as (and should not be considered to be) financial, investment or other advice on which reliance should be placed. No opinion given in the material constitutes a recommendation by EBC or the author that any particular investment, security, transaction or investment strategy is suitable for any specific person.