Published on: 2026-04-10

Updated on: 2026-04-10

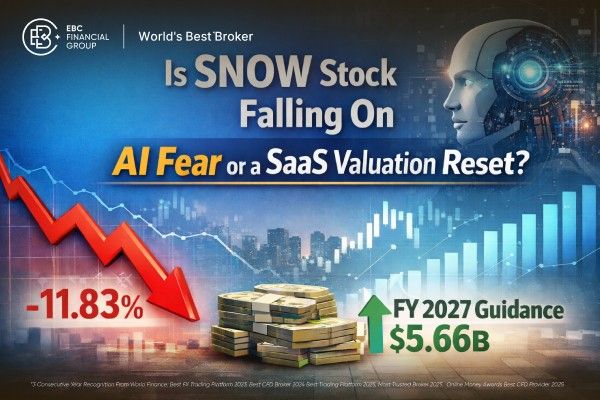

SNOW stock closed at $132.24 on April 9, 2026, down 11.83%, but the selloff occurred during a broader software-sector drawdown, not a broad-market liquidation.

The primary concern was the impact of AI, heightened by Anthropic's recent product cycle and increasing worries that AI agents could erode traditional SaaS pricing power.

Snowflake's own fiscal 2026 numbers do not yet show a same-company demand break: Q4 revenue was $1.28 billion, product revenue was $1.23 billion, and remaining performance obligations reached $9.77 billion, up 42% year over year.

Snowflake's $9.77 billion in RPO represents about 2.2 years of FY2026 product revenue, which does not align with a business experiencing immediate displacement.

Management also reaffirmed FY2027 guidance on March 31, 2026, including $5.66 billion in full-year product revenue.

SNOW stock is declining as the market reassesses software risk. On April 9, Snowflake fell 11.83% to $132.24, but this drop occurred alongside broader gains in the market and another round of AI-driven selling in software stocks. This suggests a sector-wide reevaluation rather than a company-specific collapse.

The market narrative now focuses on Anthropic's recent product launches, such as Claude Managed Agents and the limited release of Claude Mythos Preview, which have increased investor concerns about AI-native competition. There is apprehension that autonomous agents could disrupt the workflow, seat, and productivity layers that have historically supported premium SaaS valuations.

Snowflake was affected by this trend. However, its recent results indicate sustained enterprise demand rather than early signs of disruption.

The software selloff on April 9 was broad. Barron's reported the iShares Expanded Tech-Software Sector ETF fell 3.8%, while Investopedia cited a 4% drop and described the move as part of a fresh AI shock to software valuations. MarketWatch went further, calling the move a "full-fledged breakdown" and noting that names such as Okta and Zscaler fell more than 10%.

This context changes the interpretation of the day's price movement. If a stock drops 11% while the index also declines sharply, it often reflects general risk aversion.

However, if a stock falls 11% while the Nasdaq rises, the cause is typically more specific. For Snowflake, this suggests investors are adjusting their expectations for future software cash flows in an AI-focused market, indicating a valuation reset.

Our analysis shows the market is pricing in potential future risks faster than Snowflake's financials currently indicate.

Even after the decline, Snowflake's market capitalization was approximately $93.1 billion. With projected FY2027 product revenue of $5.66 billion, this equates to a valuation of about 16.5 times forward product revenue, which is high by mature software standards. The stock retained significant valuation premium even without a fundamental downturn.

Another factor challenging the AI-disruption thesis is Snowflake's active participation in AI development. In its Q4 release, the company reported over 9,100 accounts using Snowflake AI features, about 2,500 accounts adopting Snowflake Intelligence within three months, and expanded native model access through partnerships with Anthropic, Google Cloud, and OpenAI.

While strategic risks remain, this indicates Snowflake is actively engaging in the AI ecosystem rather than only defending its position.

| Metric | Latest Reported Figure | Why It Matters |

|---|---|---|

| Q4 FY2026 Revenue | $1.28 billion | Revenue still grew 30% year over year |

| Q4 FY2026 Product Revenue | $1.23 billion | Core consumption business remains solid |

| Remaining Performance Obligations | $9.77 billion | Best long-duration demand signal |

| RPO Growth | 42% YoY | Faster than revenue growth |

| FY2026 Product Revenue | $4.47 billion | Confirms full-year scale and durability |

| FY2027 Product Revenue Guidance | $5.66 billion | Management still sees growth ahead |

Snowflake's fiscal 2026 reporting does not support the idea of an immediate collapse in fundamentals.

Snowflake reported fourth-quarter revenue of $1.28 billion, up 30% year over year. Product revenue reached $1.23 billion, also up 30%, and exceeded consensus expectations by about 2.4%. These results challenge the claim that customers are already reducing spending due to AI substitution.

The key metric is RPO, which reached $9.77 billion. Remaining performance obligations represent contracted business not yet recognized as revenue. For Snowflake, RPO grew 42% year over year in Q4, up from 37% in Q3, indicating accelerating backlog growth despite negative market sentiment.

Management's position supports this view. In February, Snowflake projected $5.66 billion in product revenue for fiscal 2027 and reaffirmed this guidance for both the first quarter and full year on March 31, 2026. If significant AI disruption were already affecting demand, such reaffirmation would be difficult to justify.

The bearish perspective is reasonable. If AI agents reduce demand for certain analytics, workflow, and application layers, software valuations should adjust downward before revenue declines. The market often anticipates such threats.

For Snowflake, the key indicators to watch are RPO growth, net revenue retention, and whether FY2027 guidance holds as the year progresses.

If these indicators weaken significantly, the current selloff could shift from a valuation reset to a more substantial fundamental repricing. At present, such weaknesses are not evident in the latest reported figures.

SNOW stock declined as part of a broader software market selloff, driven by increasing concerns about potential disruptions from artificial intelligence. While the overall market was positive, software stocks weakened as investors reconsidered future SaaS margins, pricing power, and competitive advantages in an agent-driven environment.

No. Snowflake reported $1.28 billion in Q4 revenue, $1.23 billion in product revenue, and $9.77 billion in RPO, with management reaffirming fiscal 2027 guidance on March 31. These figures do not indicate immediate demand disruption.

RPO is the most important metric because it captures contracted future revenue.

In summary, Snowflake's stock decline is mainly the result of a reassessment of SaaS valuations, rather than evidence of specific AI-driven disruption to the company.

Snowflake's recent results continue to show revenue growth, an accelerating backlog, increased AI adoption on its platform, and reaffirmed fiscal 2027 guidance.

Unless Snowflake's key financial metrics worsen, current evidence more strongly supports the view that sector-wide reevaluation, not company-specific weakness, is driving the recent selloff.

Disclaimer: This material is for general information purposes only and is not intended as (and should not be considered to be) financial, investment, or other advice on which reliance should be placed. No opinion given in the material constitutes a recommendation by EBC or the author that any particular investment, security, transaction, or investment strategy is suitable for any specific person.