Published on: 2026-04-08

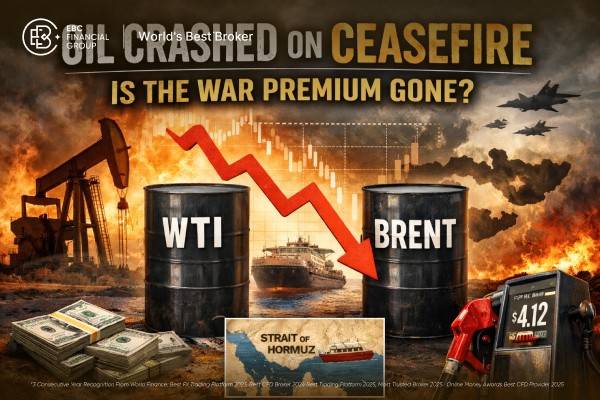

Oil crashed because the market quickly removed the highest-cost part of the geopolitical premium: the fear of a prolonged shutdown in the Strait of Hormuz.

Even after the drop, WTI still traded about $24 above the pre-war level near $73, so a meaningful part of the geopolitical premium remained embedded in price.

The latest OPEC+ increase for April is only 206,000 barrels a day, which is tiny against official estimates of 7.5 million barrels a day of March shut-ins and 9.1 million in April.

U.S. commercial crude stocks rose to 461.6 million barrels in the week ending March 27, while gasoline days of supply slipped to 27.1, which helps explain why pump-price pressure can outlast the first crude selloff.

U.S. regular gasoline averaged $4.12 a gallon on April 6, while diesel reached $5.64. That means even if crude cools further, consumer relief can lag because product markets remain tight.

The market did not suddenly become comfortable with Middle East supply. It repriced the odds of the worst-case transport shock. That distinction matters.

Oil crashed on ceasefire headlines because energy traders were pricing a shipping shock, not a collapse in demand. When the market believed the Strait of Hormuz could reopen and stay open, the most extreme shortage scenario stopped looking like the base case.

That single change was enough to knock WTI down 14.3% to $96.83 and Brent down 13.3% to $94.74 in one session, after crude had traded above $117 during the conflict spike.

The deeper question is whether the war premium has disappeared or only been repriced. The answer is the second one. The Strait of Hormuz still handles about one-fifth of global oil and petroleum product consumption and roughly one-quarter of seaborne oil trade, so even a temporary reopening does not instantly restore normal freight, insurance, or export behavior.

| Brent crude price map | Level |

|---|---|

| Pre-conflict reference, Feb. 27 | $71.00/b |

| Peak panic, Apr. 2 | ~$128.00/b |

| Post-ceasefire, Apr. 8 | $94.74/b |

| Drop from peak | $33.26/b |

| Share of spike erased | 58.4% |

| Premium still above Feb. 27 | $23.74/b |

| Share of full spike still left | 41.6% |

*This framework is based on official and market-reported price points from late February through April 8.

The table shows that the market has removed more than half of the extreme war pricing, but it has not removed the full premium. In plain terms, the panic premium is largely gone. The disruption premium is not.

A cautious working estimate is that roughly $15 to $25 a barrel of geopolitical and logistics premium is still embedded in Brent.

That range aligns three points in the latest U.S. Energy Information Administration outlook: pre-war oil fundamentals were soft, inventories were expected to build, and the ceasefire still leaves shipping control, insurance terms, and regional security unresolved.

Official energy forecasts still assume production shut-ins remain large through April and only gradually ease afterward. Those same forecasts kept a risk premium in crude through the outlook period.

They projected Brent averaging $115 a barrel in the second quarter before easing later in the year if disruptions fade.

OPEC+ agreed to raise production by 206,000 barrels a day in April. Against 9.1 million barrels a day of estimated April shut-ins, that covers barely 2.3% of the lost supply.

Even against the March shut-ins of 7.5 million barrels a day, it offsets only about 2.7%. That is a stabilizing signal, but it is not a replacement mechanism.

In EIA data for the week ending March 27, commercial crude stocks climbed to 461.6 million barrels, and crude days of supply reached 28.2, but gasoline days of supply were only 27.1, and distillate days of supply were 29.3.

That helps explain why retail fuel prices can stay firm even after crude oil futures sell off. U.S. regular gasoline averaged $4.12 a gallon on April 6, while diesel reached $5.64.

As of March 31, non-commercial traders in WTI physical futures held 378,087 long contracts against 164,599 short contracts, leaving a net long position of about 213,488 contracts.

Brent's positioning looked less supportive. In Brent last-day futures, non-commercial traders held 69,891 long contracts and 105,706 short contracts, a net short position. That contrast helps explain why a market with heavy WTI length could fall quickly once the initial headline risk began to fade.

The remaining premium disappears only if three conditions are met:

Hormuz needs sustained and broad passage, not a two-week political window.

Blocked oil supplies in the Middle East need to come back to the market more quickly than current projections suggest.

The shipping backlog must clear without new attacks, revised toll structures, or selective access rules.

Until then, crude can fall further, but it is unlikely to trade like a normal oversupplied market.

That is why the latest EIA outlook still keeps Brent elevated after flows resume. It assumes Brent peaks at $115 a barrel in the second quarter of 2026, averages $88 in the fourth quarter, and averages $76 in 2027, because uncertainty around future supply disruptions does not disappear overnight.

That indicates the market perceives a lasting impact, not just a temporary shock.

No. While more than half of the panic spike has been erased, Brent crude oil is still approximately $24 a barrel higher than its level on February 27.

Because the market had priced a prolonged closure of Hormuz, a two-week ceasefire and reopening path removed the most extreme supply-loss scenario in one move.

Not necessarily. Retail fuel prices usually lag changes in crude oil prices, and the market for fuel products remains tight. As of April 6, U.S. regular gasoline averaged $4.12 per gallon, while diesel was $5.64, reflecting refinery margins and ongoing supply constraints beyond the crude market itself.

The ceasefire broke the vertical part of the oil rally, but it did not restore a pre-war market. The significant decline in Brent indicates that traders no longer anticipate the worst-case scenario of the crisis.

The fact that crude still sits far above its late-February base says the market does expect lasting friction in shipping, inventories, and regional security.

Our read is that the panic premium is gone, while the war premium has only been cut down to size.

Disclaimer: This material is for general information purposes only and is not intended as (and should not be considered to be) financial, investment or other advice on which reliance should be placed. No opinion given in the material constitutes a recommendation by EBC or the author that any particular investment, security, transaction or investment strategy is suitable for any specific person.