Published on: 2025-09-18

Updated on: 2025-09-18

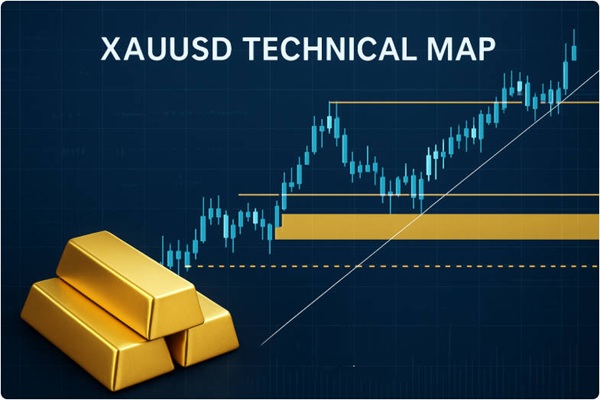

Gold rose above above $3,700 earlier this week, supported by expectations of Fed rate cut. Global stocks hit a fresh record high as US and Chinese officials discussed trade in Madrid.

A deal has been reached for social media platform TikTok, said Treasury Secretary Scott Bessent. Trump told CNBC in an interview last year that he believed the Chinese app was a national security threat.

China's market regulator on Monday said that Nvidia violated anti-monopoly law, according to a preliminary probe, adding that Beijing would continue its investigation into the chip giant.

That signals a tech war between Beijing and Washington may well drag on, though the world's two largest economies are both prioritising financial stability and therefore steering away from an all-out trade war.

What also supports animal spirits is that Europe will impose high secondary tariffs on China immediately as requested by Washington given the bloc's dependency on Chinese imports.

Global equity funds drew net outflows in the week by 10 September, while bond funds posted a 21st straight week of net inflows and money markets remained in favour, data from LSEG Lipper showed.

The federal government's budget deficit reached $2 trillion for the current fiscal year, according to CBO. Even so, benchmark 10-year Treasury yield is within a whisker of 4%, the lowest level in more than 5 months.

JP Morgan Global Research sees global core inflation increasing to 3.4% in the second half of 2025. It expects a synchronized downshift in global growth to 1.4% and central bank easing across the board.

Tariffs' impact on consumer prices will finally kick in, which could push US core inflation higher. Elsewhere, there could be a slide in European core inflation as wage pressures seem abating.

That means US real interest rate will likely continue to outstrip that of Europe by the year end, setting the dollar up for a rebound after the US Dollar Index declined more than 10% so far.

Trade deficit in goods widened sharply in July as imports surged on frontloading in the run-up to new trade policy. Market will zero in on if more balanced trade can be delivered as promised afterwards.

Pass-through from the tariffs to consumer prices has started to show up, but has been limited as many companies absorb at least part of the duties for now. As such consumer spending is not particularly a concern.

While demand for labour is softening, supply is also disappearing amid the Trump administration's immigration crackdown. The complication means policymakers will remain cautious on more cuts.

The GDPNow model estimate for Q3 growth is 3.1%, compared to the final reading of 3.3% for the previous quarter. An economy on solid footing technically bolsters demand for its currency.

A stronger dollar bodes ill for bullion, especially with the metal deep in the overbought territory. The exception is that the two tend to rise in tandem if geopolitical strain increases.

The anomaly occurred in 2023 and 2024 as the conflicts in Europe and the Middle East drove safe-haven demand for both gold and the dollar. Traders now largely shrug off the related headlines.

Russia's oil pipeline monopoly Transneft warned in August producers they may have to cut output following Ukraine's drone attacks on critical export ports and refineries, according to industry sources.

The country's central bank cut its benchmark interest rate by 100 bps on Friday to prop up a cooling wartime economy. Crude oil sentiment has swung to lower prices, probably one of the reasons of larger-scale Russia attacks.

Besides ongoing deglobalisation could cap bullion's anticipated retreat. In recent years, emerging market countries have significantly increased the use of their local currencies in international transactions.

The greenback's share of global currency reserves reported to the IMF nudged lower to 57.7% in Q1 while the share of euro-denominated reserves gained.

Global central banks bought net 10 tons of gold in July based on reported data. Despite slower pace of buying, they remain positive even in the current price range amid signs of another Cold War.

Disclaimer: This material is for general information purposes only and is not intended as (and should not be considered to be) financial, investment or other advice on which reliance should be placed. No opinion given in the material constitutes a recommendation by EBC or the author that any particular investment, security, transaction or investment strategy is suitable for any specific person.

World's Best Broker