Published on: 2026-05-15

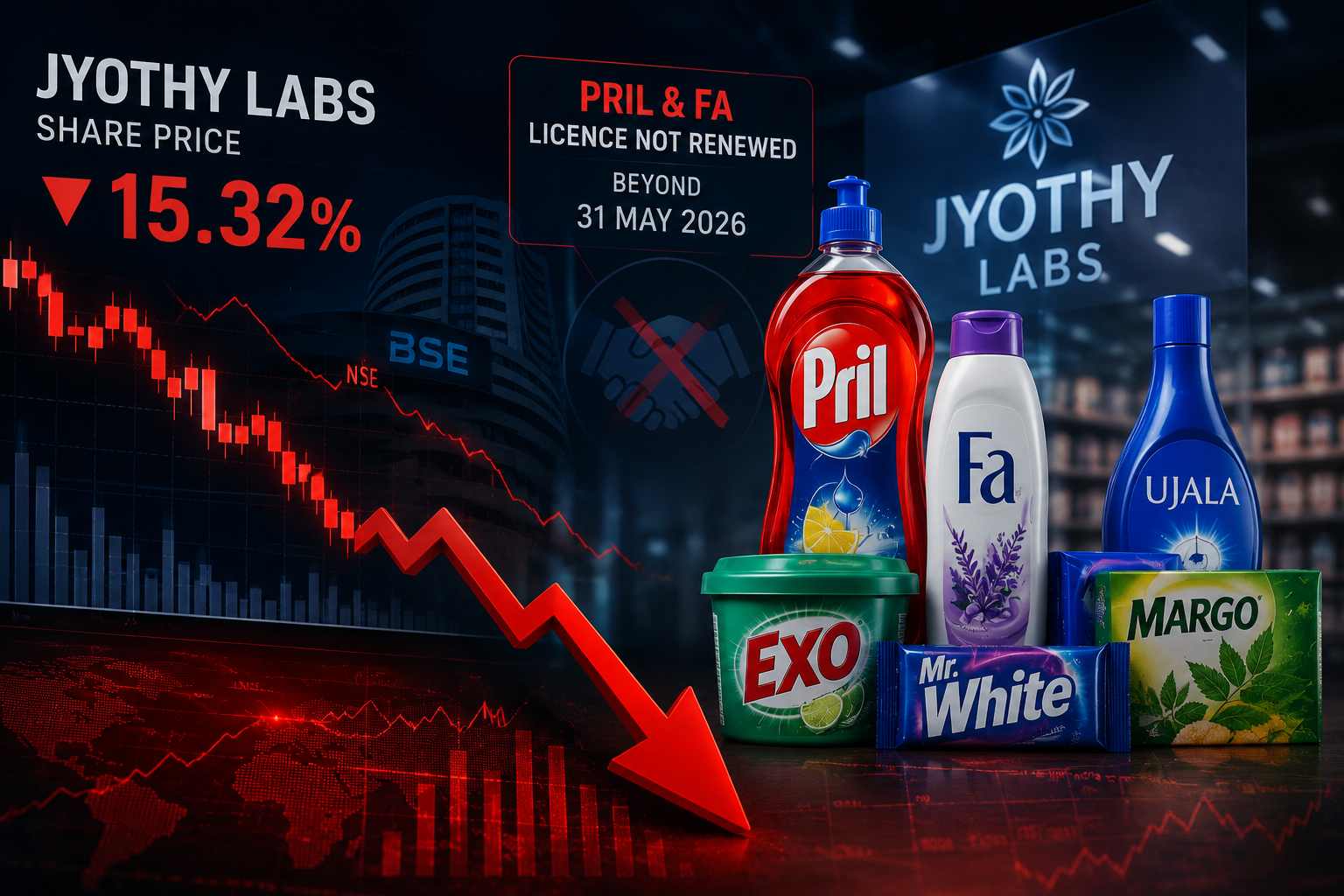

The Jyothy Labs share price was trading around ₹221 on 14 May 2026, after falling roughly 15% over two trading sessions and more than 36% over one year. If you had not been following the company closely, the speed of the fall might have looked like a panic overreaction. It was not. The market was repricing a very specific and measurable risk: what happens to Jyothy’s earnings when Pril leaves the portfolio after 31 May 2026?

To understand the answer, you have to understand what Pril actually is inside this company, and why it is not just another brand name on a shelf.

Jyothy Labs shares fell sharply after Henkel declined to renew the Pril and Fa licence agreements beyond 31 May 2026.

Pril is the bigger issue because it sits inside Jyothy’s dishwashing segment, which formed 31% of Q4 FY26 business share.

Analyst estimates suggest Pril and Fa together contribute a high single-digit share of revenue and about 10% of EBITDA, but Jyothy Labs has not confirmed exact financial exposure.

Q4 FY26 results already showed margin pressure, with EBITDA margin falling to 13.5% from 16.8% a year earlier.

Exo dishwash becomes the main replacement engine, especially in liquid dishwash, where Pril had been the anchor brand.

The balance sheet provides some support, with cash and investments near ₹997 crore, but the market is still repricing FY27 and FY28 earnings risk.

On 9 May 2026, Jyothy Labs filed with the exchanges that Henkel AG & Co. KGaA had decided not to renew the licence agreement for the Pril dishwash brand beyond 31 May 2026.

The company disclosed it had been in discussions with Henkel over renewal and alternative arrangements, but concluded there was “no further reasonable possibility” of continuation. The filing also noted that the financial impact was still under evaluation, which in market terms means no one yet knows exactly how much earnings will be affected.

The Fa personal-care brand was included in the same non-renewal. But the market reaction was disproportionately concentrated on Pril, and for good reason.

The company later clarified that Pril and Fa were fixed-term brand licence agreements, while Mr. White and Henko continue under perpetual licence arrangements with no royalty obligations. Brands such as Margo, Neem Toothpaste, Tuhina and Chek remain fully owned by Jyothy Labs.

Dishwashing is one of Jyothy’s largest product categories, contributing approximately 31% of its category-wise business share as of Q4 FY26. Within that dishwashing portfolio, Pril has been the anchor brand in liquid dishwash, the premium, higher-growth and higher-margin end of the category, while Exo anchored the bar segment.

Analysts at Equirus Securities estimated that Pril and Fa together contribute a high single-digit share of consolidated revenue, with Pril alone accounting for roughly 9% of total revenue.

More importantly, liquid dishwash carries a better margin profile than bars, so the EBITDA impact is estimated to be disproportionately larger, somewhere around 10% of company EBITDA.

This is the key point that explains the severity of the market reaction. Investors were not simply reacting to the loss of a logo. They were recalculating earnings for FY27 and FY28 with a meaningful hole where Pril’s contribution used to sit, at a time when Jyothy’s margins were already under pressure.

The Pril/Fa announcement landed when Jyothy Labs was already facing cost pressure. Q4 FY26 revenue from operations grew, but EBITDA and PAT declined as gross margins compressed.

| Metric | Q4 FY26 | YoY Change | Why It Matters |

|---|---|---|---|

| Revenue from operations | ₹717 crore | +7.7% | Demand held up despite uneven consumption |

| Volume growth | 10.8% | Positive | Growth was volume-led, not only price-led |

| Operating EBITDA | ₹96.8 crore | -13.7% | Cost pressure reduced operating leverage |

| PAT | ₹67.5 crore | -12.3% | Earnings fell despite revenue growth |

| Gross margin | 45.2% | Down from 49.2% | Input-cost inflation hit profitability |

| EBITDA margin | 13.5% | Down from 16.8% | Margin pressure was already visible |

For FY26, revenue rose 3.5% to ₹2,944 crore, while operating EBITDA fell 10% to ₹449.9 crore and PAT declined 10.2% to ₹333.2 crore. Gross margin for the full year fell to 47.0% from 50.2%.

The operating picture is therefore mixed. Jyothy Labs delivered volume growth, but revenue growth did not translate into stronger profit growth. The market’s concern is that the Pril exit could extend the margin reset into FY27 and FY28.

Jyothy Labs’ strategic response is to scale Exo dishwash across formats. The company said Pril had historically been the anchor brand in liquids, while Exo was stronger in bars. It now plans to strengthen Exo as a broader dishwash franchise spanning bars, rounds and liquids.

This gives Jyothy Labs a practical route to defend distribution, shelf space and brand salience. Exo is not a new launch. The company said Exo liquid has been part of its portfolio since 2005–06 and will now receive renewed focus and investment.

The challenge is execution. Exo has stronger recognition in dishwash bars, while Pril carried stronger positioning in liquids. Replacing Pril therefore means rebuilding not only sales volume, but also liquid-dishwash economics, channel strength and consumer recall.

Jyothy shares opened on 11 May at roughly ₹252, fell intraday by more than 9% to 11% through the session, and continued declining over the next day. By 12 May, the shares were around ₹225 during trade. By 14 May, they had settled near ₹221.

The 52-week range now spans from a high of about ₹378 to a low of ₹196.15, meaning the shares are trading well below their one-year peak and uncomfortably close to the 52-week floor.

At these levels, the market is effectively doing two things simultaneously. First, it is pricing in the Pril revenue and margin loss for FY27.

Second, it is asking whether Jyothy’s other structural pressures, namely input-cost inflation, the pace of Exo’s premiumisation, and competitive intensity from HUL’s Vim, will resolve over the same period or compound the problem.

The trailing PE is now in the low-to-mid 20s across market-data platforms, reflecting a market that still assigns value to Jyothy’s recovery potential but is no longer willing to pay for a smoother growth path without clearer execution.

A year ago, the shares were priced for a cleaner earnings trajectory. That path now has a visible obstacle.

The main risk is the FY27 and FY28 earnings gap. Analysts cited by Business Standard estimated a possible 6–8% cut in FY27 revenue assumptions and a sharper 14–16% EBITDA impact, reflecting the stronger margin profile of liquid dishwash versus bars.

Competition is another pressure point. Larger FMCG rivals have deeper advertising budgets and stronger modern-trade leverage. If Jyothy Labs needs to spend aggressively behind Exo liquid, margin recovery may take longer.

Input costs also remain a constraint. Jyothy’s FY26 presentation said margins were likely to remain subdued in the near term because of limited ability to fully pass on input-cost inflation.

Jyothy Labs shares fell after Henkel decided not to renew the Pril and Fa licence agreements beyond 31 May 2026. The market focused on Pril because it is linked to Jyothy’s important liquid dishwash business.

Jyothy Labs has not confirmed the exact impact. Analyst estimates suggest Pril and Fa may contribute a high single-digit share of revenue and around 10% of EBITDA.

Jyothy Labs plans to strengthen Exo dishwash across formats, including liquids. Exo already exists in the portfolio, but replacing Pril’s liquid-dishwash scale and margin profile may take time.

Jyothy Labs is not a company in financial distress. It carried cash and investments of approximately ₹997 crore as of its FY26 presentation and remains debt-free. FY26 volume growth was still positive, and the core brand base, including Ujala, Henko under perpetual licence, Margo, Maxo and Exo, remains intact. The business that existed before Pril will still be there after 31 May.

The question for the coming quarters is tighter: how quickly can Exo liquid gain shelf presence and consumer adoption in the premium dishwash segment that Pril is vacating? Can Jyothy stabilise gross margins as input-cost pressures ease? And will FY27 guidance, when it comes, be conservative enough to avoid a second round of downward estimate revisions?

The share price fall is best understood as a transition-risk repricing, not a collapse in the wider business. Jyothy is losing a meaningful licensed brand in an important profit pool, and the market will need evidence that Exo can close the gap without forcing a prolonged reset in margins.