Published on: 2026-02-25

Updated on: 2026-02-25

Financial markets can generate strong returns, but they can also erase years of gains during periods of uncertainty. Market crashes, inflation shocks, and sudden volatility remind traders and investors of one critical truth: avoiding large losses is often more important than chasing high returns.

This is where capital preservation becomes essential. For beginner and intermediate traders especially, protecting investment capital determines whether they can stay in the market long enough to benefit from future opportunities.

Capital preservation focuses on managing risk intelligently so portfolios remain stable during downturns while still supporting long-term wealth growth.

Capital preservation is an investment approach focused on protecting the original value of invested money while minimizing the risk of significant losses. Simply put, the primary goal of capital preservation is not losing money, rather than maximizing profits.

A capital preservation strategy typically emphasizes low-risk investment strategies, careful asset allocation, and disciplined risk management in investing. This approach is commonly used by investors nearing retirement, conservative traders, institutions managing large funds, and anyone focused on protecting investment capital.

Capital preservation works through structured decision-making designed to reduce exposure to major losses while maintaining reasonable risk-adjusted returns.

Capital preservation begins before entering any investment. Investors first establish clear risk boundaries by deciding:

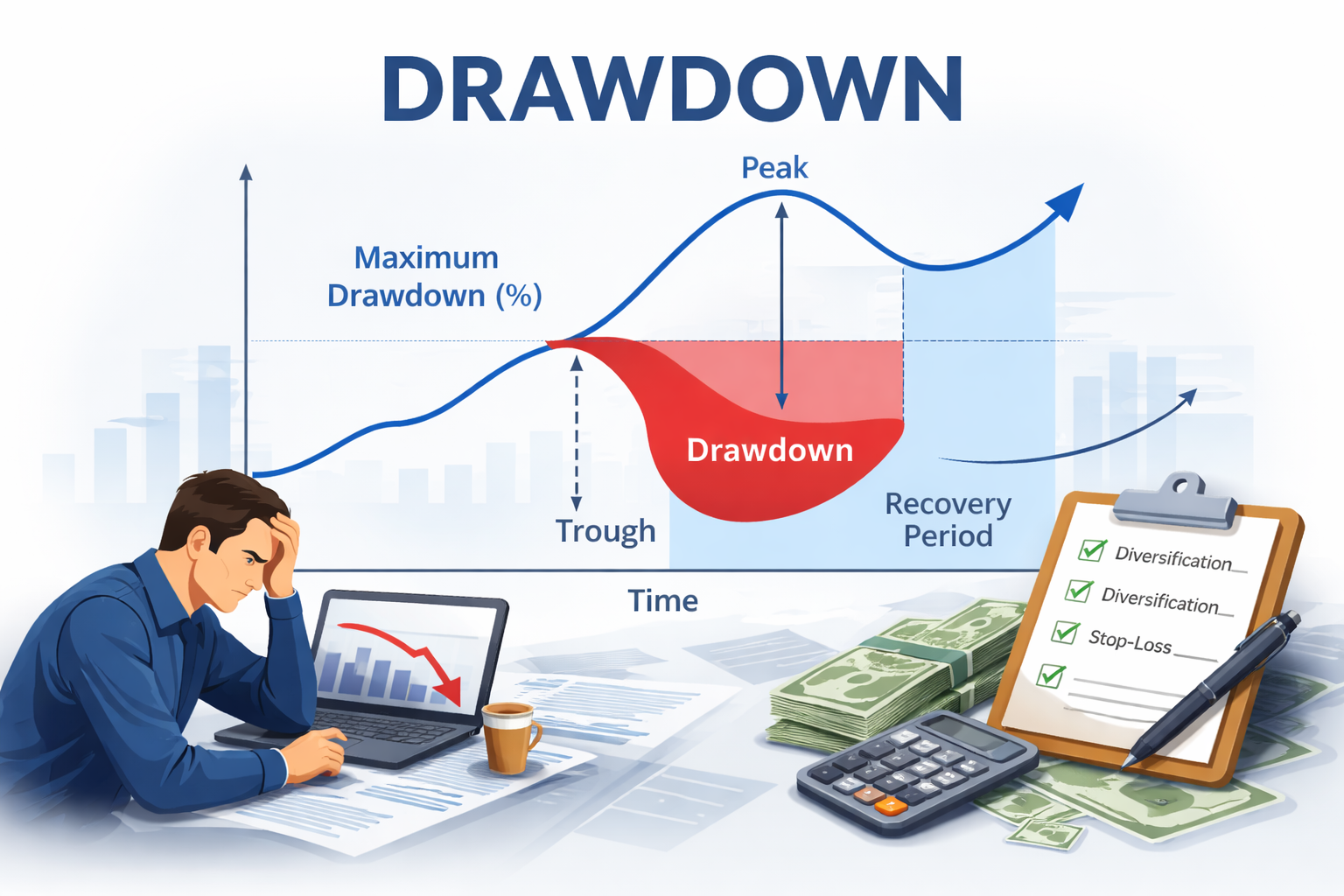

Maximum portfolio drawdown they can tolerate (e.g., 10–20%)

Risk per trade or position

Time horizon for the capital

Liquidity needs

This step prevents emotional decision-making during market stress because risk limits are defined in advance.

Rather than concentrating capital in a single opportunity, investors spread exposure across assets that behave differently under market conditions.

A preservation-focused allocation often includes:

Fixed-income securities for stability

Cash or short-term instruments for flexibility

Defensive equities for moderate growth

Inflation hedges such as commodities or real assets

The goal is not eliminating volatility entirely, but ensuring that no single market event can severely damage total capital.

One of the most powerful capital preservation tools is position sizing.

Instead of investing equal dollar amounts everywhere, investors limit how much capital is exposed to any single idea.

Common approaches include:

Risking only 1–2% of total capital per trade

Scaling into positions gradually

Avoiding oversized allocations to high-volatility assets

Small controlled losses are manageable; oversized losses can permanently impair portfolios.

Capital preservation prioritizes loss control over profit maximization.

Investors actively reduce exposure when risk increases by:

Using predefined exit levels or stop losses

Rebalancing portfolios periodically

Reducing leverage during volatile markets

Shifting toward defensive assets when uncertainty rises

This creates a defensive response system rather than reacting emotionally to market movements.

Preserving capital means maintaining purchasing power, not just avoiding nominal losses.

Investors therefore include assets capable of keeping pace with inflation, such as:

Dividend-growing equities

Inflation-linked bonds

Real assets or commodities

Broad diversified funds

A portfolio that stays flat while inflation rises is effectively losing value in real terms.

Principal: The original amount of money invested before any gains or losses occur.

Low-risk assets: Investments that are generally less likely to experience large losses or sharp price fluctuations.

Volatility: A measure of how much an investment’s price rises and falls over time.

Defensive strategy: An investment approach focused on protecting capital and reducing risk rather than maximizing growth.

Capital loss: A decrease in investment value resulting in losing part of the original money invested.

Imagine two investors each starting with $100,000.

Invests entirely in high-growth stocks.

Portfolio falls 40% during a market downturn.

Value drops to $60,000.

To recover, the portfolio now needs a 67% gain, not 40%.

Diversifies into bonds, defensive assets, and equities.

Portfolio declines only 10%.

Value becomes $90,000.

Recovering from a 10% loss requires only an 11% gain.

This example highlights why drawdown management is central to capital preservation investing: smaller losses make recovery significantly easier.

Capital preservation is what allows traders to remain active in the market long enough to benefit from opportunities. Markets are inherently volatile, and even strong strategies experience losing periods. Traders who control downside risk avoid catastrophic drawdowns that can permanently remove them from trading, forcing them to recover from survival-threatening losses instead of focusing on future opportunities.

Most professional investors operate under a simple priority: protect capital first, pursue growth second. This approach allows compounding to work effectively over time, since large losses interrupt growth far more than modest gains accelerate it. For traders, it is about building a sustainable framework that supports long-term participation and steady progress.

Capital preservation investing still seeks returns but with controlled risk. The goal is steady growth with reduced downside exposure.

While popular among retirees, traders of all experience levels use defensive strategies during uncertain market conditions.

Holding only cash exposes investors to inflation risk. True preservation balances safety with preserving purchasing power.

Every investment carries risk. Capital preservation reduces probability and severity of losses but cannot eliminate risk entirely.

Portfolio diversification reduces risk but does not fully prevent losses during systemic market events.

The main objective is protecting the original investment value while achieving modest returns that support long-term financial stability and reduce the risk of significant portfolio losses during market downturns.

Yes. Beginners benefit greatly because preserving capital allows more time to learn, adapt strategies, and avoid early large losses that can permanently reduce trading opportunities.

Diversification spreads risk across different assets and sectors, reducing the impact of any single loss and improving overall portfolio stability during volatile market conditions.

They may underperform during strong bull markets but often outperform on a risk-adjusted basis over full market cycles by limiting drawdowns and protecting long-term compounding.

Common choices include government bonds, cash equivalents, dividend-paying stocks, gold, defensive sectors, and diversified funds designed to provide stability and downside protection.

Capital preservation is a foundational principle of successful investing and trading. Rather than focusing solely on profits, it prioritizes protecting investment capital through diversification, disciplined risk management, and defensive positioning.

Capital preservation investing recognizes that avoiding large losses is essential for achieving long-term wealth stability. Managing drawdowns, balancing risk exposure, and preserving purchasing power, investors create a stronger foundation for sustainable growth.

For traders and investors alike, the key takeaway is simple: markets always offer new opportunities but only those who protect their capital are able to take advantage of them over time.

Disclaimer: This material is for general information purposes only and is not intended as (and should not be considered to be) financial, investment or other advice on which reliance should be placed. No opinion given in the material constitutes a recommendation by EBC or the author that any particular investment, security, transaction or investment strategy is suitable for any specific person.

World's Best Broker